The 2015 Telemedicine Report

/ 2015 Telemedicine Report from Freelance MD

2015 Telemedicine Report from Freelance MD

The 2015 Telemedicine Report: This report provides an overview of the current sentiment and opinion of telemedicine from the point of view of tens of thousands of clinicians and health care administrators all around the world. This report provides insights into providers’ opinions and the current level of opportunity for telemedicine to have an impact on the delivery of health care.

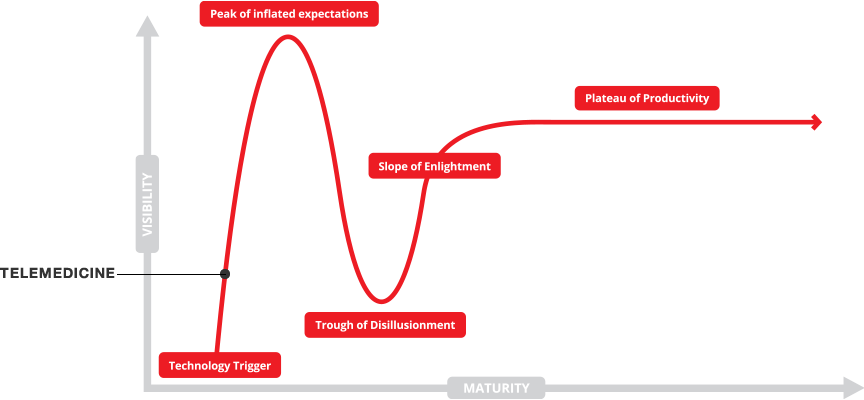

The Telemedicine Story: Telemedicine is in its infancy but poised to gain wider acceptance and usage as health care providers and markets realize its potential to both scale delivery of services and cut costs (efficiency) and drive greater revenue by removing friction from provider-patient interactions (scalability).

The current view of telemedicine is just beginning to become a topic of mainstream discussions and excitement is growing along with expectations. We're happy to have been able to work with Freelance MD to help generate the content for this report. (A special thanks for our Members who contributed.)

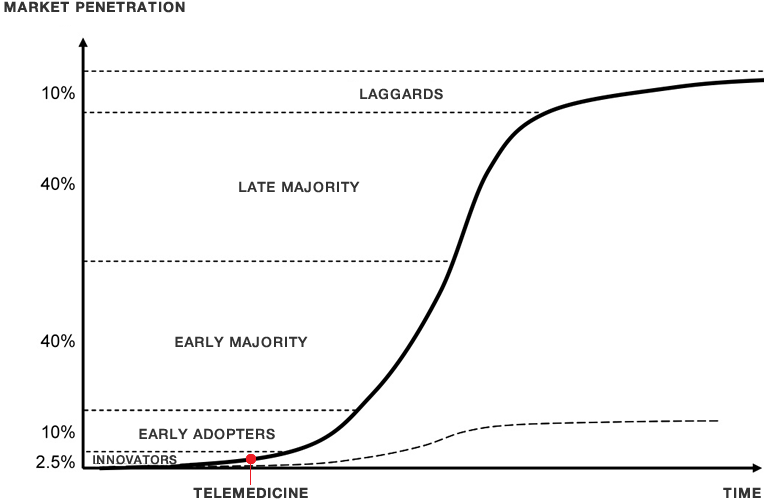

There are indications that this is beginning to happen as insurance companies and others see this as a way to provide high-value services at a more reasonable cost while keeping patients healthy and without the need for more expensive intervention treatments. For example, Arches Health Plan recently announced that it will reimburse providers for home-based telemedicine interactions. As this becomes more commonplace the few remaining impediments to adoption will be removed and telemedicine will begin to ramp from the realm of innovators and early adopters and towards the majority of providers.

Market Opportunities

As with all emerging technologies telemedicine is going to disrupt some traditional models and put others out of business. Telemedicine is inherently more efficient, more predictable, and less costly than any current delivery of care. While it cannot replace actual interventional or hands-on care, it solves entire categories of wasteful informational visits and begins to provide a platform where every provider and patient has access to the very best information and care. Early adopters are already realizing this in as evidenced by adoption trends being more pronounced in cosmetic and concierge medicine (direct pay) than family and general practice (third party payer). Those providers who get out ahead of this macro-economic trend be best situated to capitalize on what will inevitably be a commercial marketplace with both winners and losers driven by the availability of big data and consumer choice.

Make sure that you take a look at our other free reports for Members here.